How Car Insurance Payments Affect Your Credit Score

At Compare.com, it’s our mission to find simple ways to help our customers save money on the things they need. While we partner with some of the companies and brands we talk about in our articles, all of our content is written and reviewed by our independent editorial team and never influenced by our partnerships. Learn about how we make money, review our editorial standards, and reference our data methodology to learn more about why you can trust Compare.com.

You’re a good driver, so why is your car insurance premium so high? It might be your credit score — according to the Center for Insurance Policy and Research, roughly 95% of all car insurers check your credit to determine your monthly premiums. This makes achieving a high credit score critical. To keep premiums low, keep reading to learn how to improve your credit score.

If your premiums are higher than you’d like and you fear a lower credit score due to non-payment or late payment, it may be time to search for a new, more affordable insurance provider. To find the best car insurance rates, enter your ZIP code below:

Compare Rates from Dozens of Companies

What is a Credit Score?

A credit score is a numerical rating from 300 to 850 that measures a person’s creditworthiness or likelihood to repay a debt. The lowest possible score is 300 and the highest is 850. Lenders such as mortgage and leasing companies use credit scores to qualify you for loans, determine loan repayment terms, and set interest rates.

Does Paying Car Insurance Build Credit?

No, unfortunately paying your car insurance premiums doesn’t build credit, even if you never miss a payment. But your car insurance premium might be determined using your credit score as one of many determining factors. We’ll get into that in a moment.

If you miss a lot of payments, your insurance company could send your payments to a collections agency, which can stay on your credit report for up to a decade. The quickest way to poor credit is having a collection agency appear on your credit file.

There are other consequences to missed or late payments — failure to pay your insurance premiums every month can result in late fees, higher premiums, and the eventual cancellation of your policy. Insurers can cancel policies with as few as two consecutive missed payments.

Although there are no direct ties between your car insurance payments and your credit score, one way to help build credit using car insurance is to put the insurance payments on a credit card and pay the balance in full every month. On-time payments reflect well to the three major credit bureaus — Experian, Equifax, and TransUnion. Those steady payments can increase your score over time.

What Does Affect My Credit Score?

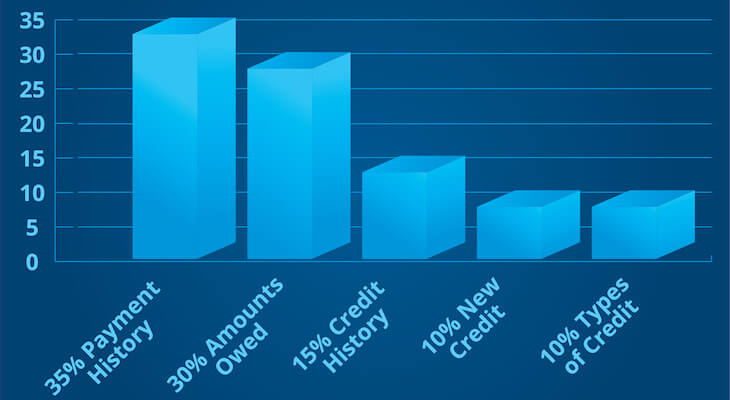

Several factors affect your credit score, including payment history, length of credit history, credit usage, credit mix, and recent activity:

- Payment history is the ratio of on-time payments to late payments made to multiple creditors (like your mortgage and credit card). One late payment can drop your credit score by 20 points or more.

- Length of credit history refers to how long you’ve held credit, so when you opened your credit cards or when you got your first loan. The older the average age of all of your credit accounts, the higher your credit score.

- Credit usage refers to how much of your available credit you’re using. This is also called credit utilization. A good credit utilization rate is traditionally considered to be 30%.

- New credit refers to new accounts and loans you have in your account. Anytime you open up a new credit card or get approved for a home or car loan, this can cause fluctuation in your scores.

- Credit mix refers to how diverse your credit products are. It’s generally smart to have a variety of credit accounts, including mortgages, credit cards, and auto loans. This is one factor that shows lenders you’re financially responsible and can be trusted to repay your debts.

According to FICO, your payment history accounts for 35% of your score. Credit utilization (which they call amounts owed), length of credit history, credit mix, and new credit follow at 30%, 15%, 10%, and 10%, respectively.

Your credit score does not factor in age, gender, race/nationality, job title, salary, or other identifying information.

What is a Credit-Based Insurance Score?

While paying car insurance doesn’t build credit, it can be the other way around: Credit can affect car insurance premiums (by a lot).

Insurers use a credit-based insurance score to predict the likelihood of risk of loss. It evaluates that risk and sets policy rates based on how likely it is that the insured will file a future claim.

In some states, having bad credit will hike your insurance rates by thousands more than a DUI will. Even if you have credit that’s considered “good,” you’ll pay $214 more per year, on average, than drivers with perfect credit.

Credit-based insurance scores determine the premiums you pay for other types of coverage (e.g., home insurance, life insurance, and renters insurance).

Like credit scores, credit-based insurance scores are calculated based on payment history, amount of outstanding debt, credit history length, credit mix, and the number of new credit applications on your record.

Credit-based insurance scores are only one factor used to determine premiums. Some of the other factors used to determine insurance premiums include age, gender, ZIP code, driving history, driving habits, vehicle type, occupation, and payment history.

Why Do Car Insurers Care About My Credit Score?

Research has shown that your credit-based insurance score is a good predictor of your likelihood of filing a claim. The lower a person’s score, the more likely you will file a claim through your insurance company.

Some consumer advocacy groups protest using credit-based insurance scores, saying that minorities are disproportionately affected and that most customers don’t understand that their credit can affect their insurance premiums. If you live in California, Hawaii, or Massachusetts, auto insurers are prohibited from checking your credit history.

Some insurers, like Nationwide, have an extraordinary life circumstances policy that allows you to request a reconsideration of your premium if your credit has suffered because of a divorce, military deployment, severe illness, or another catastrophic event.

Does My Credit Affect the Insurance Rates I Pay?

A whopping 95% of auto insurance companies use credit-based insurance scores to determine your premiums.

Furthermore, a 2003 investigation by the University of Texas at Austin discovered that $918 was the average insurance claim paid by people with the lowest credit scores versus $558 for people with the highest credit scores. It simply pays to have the highest credit possible.

What Payments Help Your Credit Score?

We recommend making timely monthly payments to all creditors that report lateness to the credit card bureaus and pursue collections activity with unpaid balances. These include (but aren’t limited to) mortgage, credit card, utility, and lending companies. Keeping a spot-free record every month will gradually increase your credit score over time.

Secondly, consider your credit utilization ratio, or the ratio between your credit card balances and limits. Aim for a target utilization of 10% or below for the greatest impact to your score.

No matter your credit mix, it’s essential to avoid late payments, defaults, and collections activity at all costs.

What Do I Do if My Credit Report is Wrong?

Occasionally, credit reports will contain the wrong information. In a Federal Trade Commission report, 25% of U.S. consumers found errors on one of their credit reports.

We recommend checking your credit report frequency for errors. These include incorrect first names, closed accounts reported as open, accounts wrongly labeled as delinquent, etc. To dispute mistakes on your credit report, contact the credit bureau(s) with the errors in question by mail with a written statement and all supporting documentation.

Here is the address for each credit bureau:

Equifax

PO Box 740256

Atlanta, GA 30374

TransUnion LLC

Consumer Dispute Center

PO Box 2000

Chester, PA 19016

Experian

PO Box 4500

Allen, TX 75013

From there, you should expect to wait 45 days for credit bureaus to provide written results of the investigation. They may keep the error intact or update/remove the error from your report. Any updates can take more than a month to appear, so don’t be alarmed if you don’t hear back promptly.

I Don’t Know My Credit Score. Where Do I Go?

Don’t pay for your credit report when you don’t have to. Federal law requires each of the three major credit bureaus to give you one free credit report each year.

You can visit AnnualCreditReport.com to request a report. We are also big fans of Credit Karma. It consolidates Equifax and TransUnion scores in an easy-to-read interface with your recent transactions by creditors (including your auto insurance carrier and dozens of other touchpoints regarding your financial health.

Shop Around for the Best Car Insurance Rates

If you experience a large increase in your score or pay higher-than-average monthly payments with little to no discounts (like safe driver discounts), it may be time to consider a new insurance provider.

Compare all of your options by entering your ZIP code below:

Unlock Your Cheapest Rates for Free

Nick Versaw leads Compare.com's editorial department, where he and his team specialize in crafting helpful, easy-to-understand content about car insurance and other related topics. With nearly a decade of experience writing and editing insurance and personal finance articles, his work has helped readers discover substantial savings on necessary expenses, including insurance, transportation, health care, and more.

As an award-winning writer, Nick has seen his work published in countless renowned publications, such as the Washington Post, Los Angeles Times, and U.S. News & World Report. He graduated with Latin honors from Virginia Commonwealth University, where he earned his Bachelor's Degree in Digital Journalism.

Compare Car Insurance Quotes

About Compare.com

Compare.com’s #1 goal is to save you money. We publish resources that are based on hard-hitting data and years of industry experience to help you make more informed decisions with your wallet.

- All of Compare.com’s content is written and reviewed for accuracy by a team of experienced writers and editors who are experts on the topics they cover.

- None of Compare.com’s content is ever influenced by the companies and brands we partner with.

- Compare.com’s editorial team operates independently of any of the company’s partnership or business development interests. We publish unbiased information strictly for the benefit of our readers.

- All of the content you see on Compare.com is based on comprehensive analysis and all data is gathered and vetted from trustworthy sources.

Learn more about us, our team, and what makes us tick.